Personal finance can seem overwhelming when you’re just getting started.

Articles, videos, and financial experts often use terms that may sound confusing if you’ve never studied finance before.

Words like assets, liabilities, inflation, equity, diversification, and net worth appear frequently, yet many beginners don’t fully understand what they mean.

Learning basic financial terminology is one of the first steps toward becoming financially literate.

Once you understand these common terms, it becomes much easier to follow financial advice, compare financial products, and make informed decisions about your money.

The good news is that you don’t need to memorize hundreds of complicated definitions.

Understanding the most commonly used financial terms provides a strong foundation for managing your personal finances with confidence.

This guide explains the essential financial terms every beginner should know using simple language and practical examples.

Essential Financial Terms at a Glance

| Financial Term | Simple Meaning |

|---|---|

| Income | Money you earn from work, business, or investments. |

| Expense | Money you spend on goods, services, or bills. |

| Budget | A plan for how you will spend and save your money. |

| Savings | Money set aside for future use. |

| Investment | Money used to purchase assets with the goal of growing wealth. |

| Asset | Something you own that has financial value. |

| Liability | Money or financial obligations you owe. |

| Net Worth | The value of your assets minus your liabilities. |

This table introduces the most common terms you’ll encounter when learning about personal finance.

Income

Income is the money you receive from various sources.

Examples include:

- Salary.

- Wages.

- Business profits.

- Freelance work.

- Rental income.

- Investment income.

Your income provides the financial resources needed to cover expenses, save money, and invest for the future.

Expenses

Expenses are the costs you pay for goods and services.

Examples include:

- Rent.

- Groceries.

- Transportation.

- Utilities.

- Insurance.

- Entertainment.

- Healthcare.

Tracking expenses helps you understand where your money goes each month and identify opportunities to save.

Budget

A budget is a financial plan that helps you manage your income and expenses.

A good budget allows you to:

- Pay bills on time.

- Control spending.

- Save consistently.

- Avoid unnecessary debt.

- Work toward financial goals.

Budgeting is one of the most important skills in personal finance.

Savings

Savings are money you intentionally set aside instead of spending.

People save money for many reasons, including:

- Emergencies.

- Vacations.

- Education.

- Home purchases.

- Retirement.

- Major planned expenses.

Savings provide financial security and reduce dependence on borrowing.

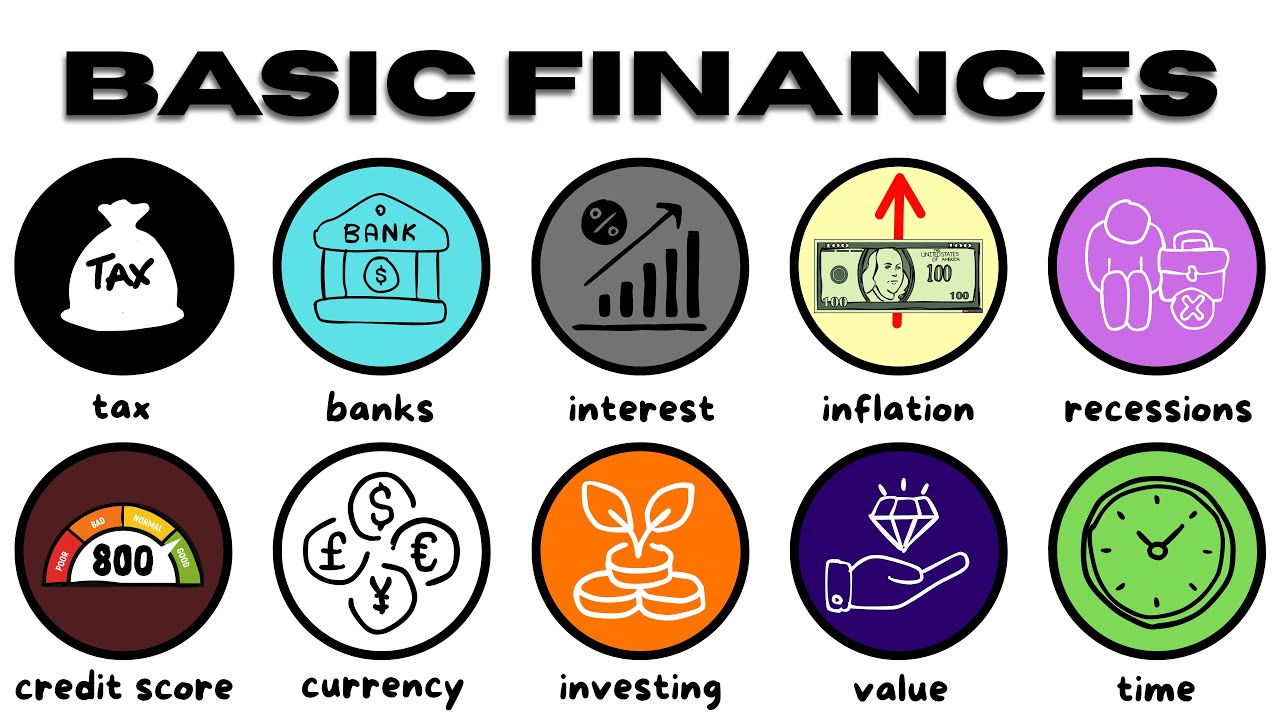

Investment

An investment is money used to purchase assets that have the potential to increase in value over time.

Common investments include:

- Stocks.

- Bonds.

- Mutual funds.

- Exchange-Traded Funds (ETFs).

- Real estate.

Unlike savings, investments involve some level of risk but may provide higher long-term returns.

Asset

An asset is anything you own that has financial value.

Examples include:

- Cash.

- Savings accounts.

- Investments.

- Real estate.

- Vehicles.

- Valuable property.

- Business ownership.

Assets contribute positively to your net worth.

Liability

A liability is money that you owe to another person or organization.

Examples include:

- Home loans.

- Car loans.

- Student loans.

- Credit card balances.

- Personal loans.

Liabilities reduce your net worth because they represent financial obligations.

Net Worth

Net worth measures your overall financial position.

It is calculated by subtracting your total liabilities from your total assets.

Tracking your net worth over time helps you monitor your financial progress and evaluate how effectively you’re building wealth.

Emergency Fund

An emergency fund is money reserved for unexpected financial situations.

Common emergencies include:

- Job loss.

- Medical expenses.

- Major home repairs.

- Vehicle repairs.

- Urgent family expenses.

Having an emergency fund helps you avoid relying on high-interest debt during difficult situations.

Interest

Interest is the cost of borrowing money or the reward for Saving and Investing.

If you borrow money through a loan or credit card, you usually pay interest.

If you keep money in certain savings or investment products, you may earn interest.

The interest rate has a major impact on how much borrowing costs and how quickly your savings can grow.

Compound Interest

Compound interest means earning interest on both your original money and the interest you’ve already earned.

Unlike simple interest, compound interest allows your money to grow faster over time because each period’s earnings begin generating additional earnings.

This is one of the main reasons financial experts encourage long-term saving and investing.

Inflation

Inflation refers to the gradual increase in the prices of goods and services over time.

As inflation rises, the purchasing power of your money decreases.

For example, an amount that buys a week’s groceries today may buy fewer items several years from now if prices continue to rise.

Understanding inflation helps you appreciate the importance of saving and investing for long-term financial goals.

Credit Score

A credit score is a numerical measure used by lenders to evaluate how responsibly you have managed borrowed money in the past.

A strong credit score may improve your ability to:

- Qualify for loans.

- Receive lower interest rates.

- Access certain financial products.

Making payments on time and managing debt responsibly are important factors in maintaining a healthy credit profile.

Debt

Debt is money borrowed with the agreement that it will be repaid, usually with interest.

Common forms of debt include:

- Credit cards.

- Home loans.

- Student loans.

- Personal loans.

- Vehicle loans.

Not all debt is harmful.

Understanding how borrowing works helps you make informed financial decisions.

Diversification

Diversification means spreading your investments across different types of assets rather than relying on a single investment.

This strategy helps reduce risk because poor performance in one investment may be balanced by stronger performance in others.

Diversification cannot eliminate risk entirely, but it can improve the stability of a long-term investment portfolio.

Liquidity

Liquidity refers to how quickly an asset can be converted into cash without significantly affecting its value.

Cash is considered highly liquid because it is immediately available for spending.

Real estate, on the other hand, is generally less liquid because selling property usually requires more time.

Understanding liquidity helps you decide where to keep money for short-term needs versus long-term goals.

Insurance

Insurance is financial protection against unexpected losses.

Depending on the policy, insurance may help cover costs related to:

- Medical treatment.

- Property damage.

- Vehicle accidents.

- Disability.

- Loss of life.

Insurance reduces financial risk rather than creating wealth.

Tax

Tax is money collected by governments to fund public services and infrastructure.

Adults should understand basic tax concepts such as:

- Taxable income.

- Tax deductions.

- Tax credits.

- Filing tax returns.

- Tax planning.

Basic tax knowledge helps you stay compliant and make better financial decisions.

Financial Terms at a Glance

| Financial Term | Why It’s Important |

|---|---|

| Interest | Determines the cost of borrowing and the return on savings. |

| Compound Interest | Helps money grow faster over long periods. |

| Inflation | Reduces purchasing power over time. |

| Credit Score | Affects borrowing opportunities and loan costs. |

| Debt | Influences financial obligations and cash flow. |

| Diversification | Helps reduce investment risk. |

| Liquidity | Indicates how easily assets can be converted to cash. |

| Insurance | Protects against unexpected financial losses. |

| Tax | Helps you understand legal financial responsibilities and planning. |

Why Learning Financial Terms Matters

Learning financial vocabulary isn’t about sounding knowledgeable—it’s about making better financial decisions.

Understanding common terms helps you:

- Read financial articles with confidence.

- Compare financial products more effectively.

- Understand investment opportunities.

- Avoid costly misunderstandings.

- Communicate more confidently with financial professionals.

- Build stronger long-term money management skills.

Every new financial term you learn makes the next topic easier to understand, creating a solid foundation for lifelong financial literacy.

Additional Financial Terms Worth Learning

Once you understand the basic financial vocabulary, you can gradually expand your knowledge with a few additional terms that appear frequently in personal finance.

Cash Flow

Cash flow is the movement of money into and out of your finances.

Positive cash flow means you earn more than you spend.

Negative cash flow means your expenses exceed your income.

Maintaining positive cash flow makes it easier to save, invest, and pay off debt.

Equity

Equity represents the portion of an asset that you truly own after subtracting any outstanding debt.

For example, if your home is worth $300,000 and your remaining mortgage is $200,000, your equity is $100,000.

As you repay debt or the value of the asset increases, your equity may grow.

Return on Investment (ROI)

Return on Investment, often called ROI, measures how much profit or loss an investment generates compared to the amount originally invested.

Investors commonly use ROI to compare different investment opportunities and evaluate financial performance.

Risk Tolerance

Risk tolerance refers to your ability and willingness to accept fluctuations in the value of your investments.

Factors that influence risk tolerance include:

- Age.

- Financial goals.

- Investment timeline.

- Income stability.

- Personal comfort with uncertainty.

Understanding your risk tolerance helps you choose investments that match your financial situation.

Passive Income

Passive income is money earned with relatively little ongoing effort after the initial work or investment.

Examples may include:

- Rental income.

- Dividend income.

- Royalties.

- Interest from certain financial products.

While passive income often requires time, capital, or effort to establish, it can become an important part of long-term financial planning.

Common Mistakes Beginners Make

Learning financial terminology is valuable, but beginners sometimes misunderstand how these terms apply in real life.

Some common mistakes include:

- Memorizing definitions without understanding practical use.

- Confusing income with wealth.

- Ignoring inflation when planning long-term finances.

- Assuming all debt is harmful.

- Investing before learning basic financial concepts.

- Believing complex financial terms automatically lead to better investments.

- Depending solely on social media for financial education.

Understanding how these terms relate to everyday financial decisions is far more valuable than simply knowing their definitions.

Tips for Learning Financial Terms Faster

Building financial knowledge doesn’t have to feel overwhelming.

These simple habits can help you learn more effectively:

- Learn a few new financial terms each week.

- Apply new concepts to your own finances whenever possible.

- Read beginner-friendly personal finance books and articles.

- Keep a personal glossary of important financial terms.

- Review unfamiliar words whenever you encounter them.

- Continue learning as your financial responsibilities grow.

Financial literacy develops gradually, and consistent learning often produces better results than trying to learn everything at once.

Frequently Asked Questions

Why should beginners learn financial terms?

Understanding financial terminology makes it easier to manage money, compare financial products, understand investments, and make informed financial decisions throughout life.

Which financial terms should I learn first?

Most beginners should start with income, expenses, budgeting, savings, investing, assets, liabilities, debt, interest, inflation, and net worth because these concepts form the foundation of personal finance.

Do I need a finance degree to understand these terms?

No.

Financial terminology can be learned through books, educational websites, practical experience, and consistent self-study.

Anyone can improve their financial literacy with regular learning.

How many financial terms should I learn at once?

Focus on learning a small number of terms at a time and understand how they apply to real-life financial situations.

Gradual learning is usually more effective than trying to memorize a large number of definitions.

Will understanding financial terms help me become better with money?

Yes.

Knowing what financial terms mean helps you understand advice, avoid common mistakes, evaluate financial opportunities, and make more confident decisions about saving, investing, borrowing, and managing your finances.

How can I remember financial terms more easily?

The best way is to use them regularly.

Reading personal finance content, tracking your own finances, and applying new concepts in everyday life will help reinforce your understanding.

Conclusion

Learning financial terms is one of the first and most important steps toward becoming financially literate.

These words are more than just definitions—they represent the concepts that shape how you earn, save, spend, borrow, invest, and build wealth throughout your life.

You don’t need to become a financial expert overnight.

Start by understanding the most common terms, apply them to your own financial decisions, and continue expanding your knowledge over time.

As your confidence grows, you’ll find it easier to evaluate financial products, avoid costly mistakes, and make smarter choices with your money.

Financial literacy is built one concept at a time, and every new term you learn strengthens the foundation for a more secure financial future.