Credit cards can be a convenient financial tool when used responsibly.

They allow you to make purchases, build a credit history, and manage short-term cash flow.

However, many cardholders make only the minimum payment each month without fully understanding the long-term consequences.

While paying the minimum amount usually helps keep your account in good standing, it doesn’t eliminate your debt.

Instead, it often extends the repayment period and increases the total amount of interest you pay over time.

For someone carrying a balance month after month, paying only the minimum can make debt much more expensive than expected.

This guide explains what minimum credit card payments are, what happens when you pay only the minimum, and how you can reduce credit card debt more effectively.

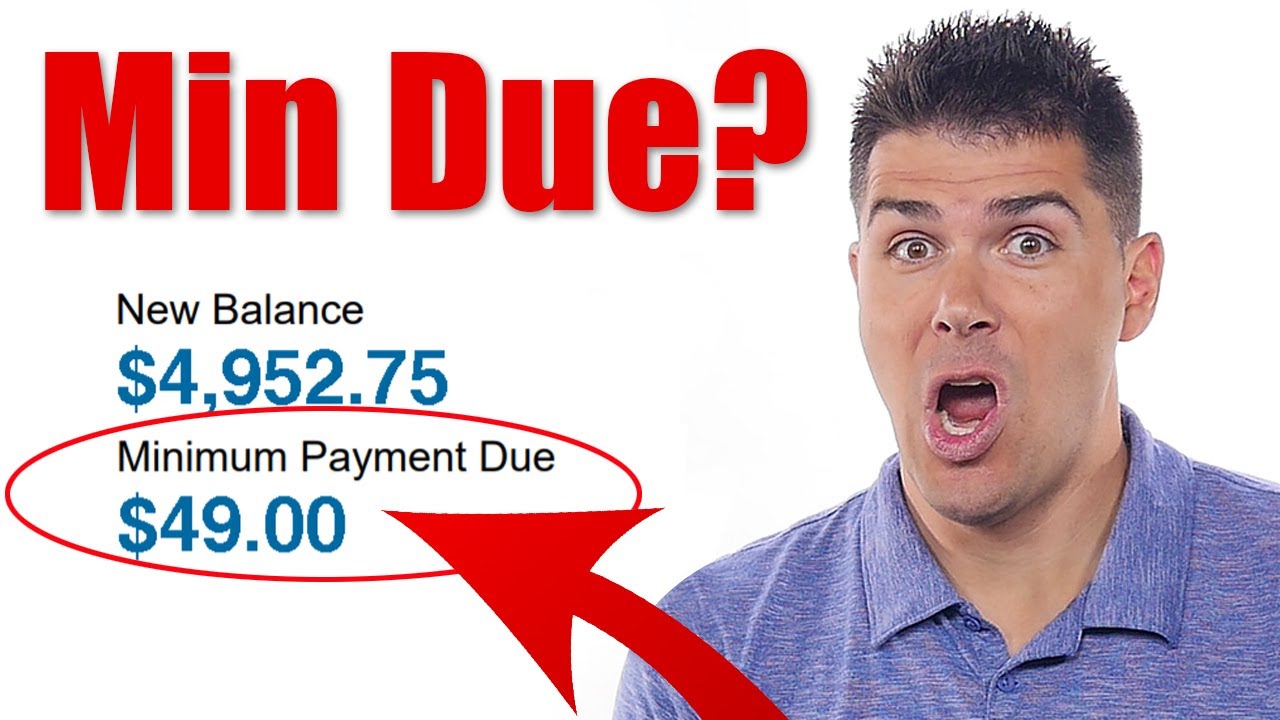

What Is a Minimum Credit Card Payment?

A minimum payment is the smallest amount your credit card issuer requires you to pay by the monthly due date to keep your account current.

The exact calculation varies by card issuer, but it is generally only a small percentage of your outstanding balance, sometimes combined with interest, fees, or other charges.

Making at least the minimum payment usually helps you avoid late payment penalties associated with missing the payment entirely.

However, paying only the minimum does not mean your balance has been paid off.

What Happens When You Pay Only the Minimum?

Although your account generally remains current, several financial consequences may occur when you repeatedly make only minimum payments.

Your Debt Takes Much Longer to Repay

Because only a small portion of your payment usually reduces the principal balance, the remaining balance continues into the next billing cycle.

As a result, it may take months or even years to eliminate the debt if you continue making only minimum payments.

You Pay More Interest

When a balance remains on your credit card, interest is generally charged according to the card’s terms.

The longer you carry the balance, the more interest you may pay.

Over time, the total interest can become a significant portion of the overall repayment cost.

Your Available Credit Remains Lower

A large outstanding balance reduces the amount of available credit remaining on your credit card.

Having less available credit may reduce your financial flexibility if unexpected expenses arise.

It Can Slow Financial Progress

Money spent on interest cannot be used for other financial priorities.

For example, continuing to carry credit card debt may reduce your ability to:

- Build an emergency fund.

- Save for retirement.

- Invest for long-term goals.

- Pay off other debts.

- Reach important financial milestones.

Reducing credit card debt can free more of your income for wealth-building activities.

Simple Example

Imagine you have a credit card balance of $2,000.

If you pay only the required minimum each month while continuing to be charged interest according to your card agreement, a significant portion of each payment may go toward interest rather than reducing the principal balance.

As a result:

- The balance decreases slowly.

- Interest continues to accumulate.

- Total repayment costs increase.

- It may take much longer to become debt-free.

This example illustrates why many financial educators recommend paying more than the minimum whenever possible.

Minimum Payment vs Paying More

| Feature | Minimum Payment | Paying More Than the Minimum |

|---|---|---|

| Monthly Payment | Lower | Higher |

| Debt Repayment Speed | Slower | Faster |

| Total Interest Paid | Usually higher | Usually lower |

| Financial Flexibility | Improves slowly | Improves more quickly |

| Long-Term Cost | Often greater | Often lower |

This comparison shows that while minimum payments help keep your account current, larger payments generally reduce debt more efficiently.

Why Credit Card Companies Allow Minimum Payments

Minimum payments provide flexibility for people who cannot pay their entire balance during a particular month.

This feature can help avoid missed payments during temporary financial difficulties.

However, relying on minimum payments over a long period may result in higher borrowing costs because interest continues to accumulate according to the card agreement.

Understanding this difference helps you use credit cards more effectively and avoid unnecessary long-term debt.

How Interest Continues to Increase Your Debt

When you don’t pay your full credit card balance, the remaining amount is generally carried forward to the next billing cycle.

Interest is then typically charged on that remaining balance according to your card agreement.

If you continue making only the minimum payment each month:

- A large portion of each payment may go toward interest.

- Only a small portion may reduce the original balance.

- Your debt decreases much more slowly.

- The total cost of borrowing increases over time.

This is one of the main reasons long-term credit card debt can become expensive.

Credit Utilization May Stay High

Credit utilization refers to how much of your available credit you’re using.

For example:

- If your credit limit is $5,000 and your outstanding balance is $4,000, you’re using a large portion of your available credit.

- If you reduce that balance significantly, your utilization decreases.

Consistently carrying a high balance may affect your overall credit profile, depending on how credit scoring models evaluate your borrowing behavior.

Reducing your balance generally lowers your credit utilization over time.

Paying More Than the Minimum Can Save Money

Even small additional payments can make a meaningful difference.

For example:

Instead of paying only the minimum required amount, imagine paying an extra amount every month.

That additional payment goes directly toward reducing your remaining balance more quickly.

As the balance decreases:

- Less interest is charged in future billing cycles.

- Your debt is repaid sooner.

- The total borrowing cost is reduced.

Consistent extra payments can have a significant long-term impact.

Practical Example

Imagine two people each have the same credit card balance.

Person A pays only the minimum every month.

Person B pays the minimum plus an additional amount whenever possible.

Over time:

- Person B’s balance decreases faster.

- Person B generally pays less total interest.

- Person B becomes debt-free sooner.

- Person A remains in debt for a longer period.

Although both individuals make their required payments, paying more than the minimum usually produces better financial outcomes.

When Paying Only the Minimum May Be Necessary

Sometimes paying only the minimum is unavoidable.

Examples include:

- Temporary job loss.

- Medical emergencies.

- Unexpected household expenses.

- Short-term financial hardship.

In these situations, making at least the required minimum payment can help you avoid missing a payment while you work to stabilize your finances.

Once your financial situation improves, increasing your monthly payments can help reduce the remaining balance more quickly.

Strategies to Pay Off Credit Card Debt Faster

If your goal is to eliminate credit card debt, consider these practical strategies:

- Pay more than the minimum whenever your budget allows.

- Stop adding new charges while paying down existing balances.

- Create a realistic monthly budget.

- Reduce unnecessary discretionary spending.

- Use unexpected income, such as bonuses or tax refunds, to Make additional payments.

- Prioritize high-interest debt if you have multiple outstanding balances.

- Track your progress to stay motivated.

Even modest additional payments can reduce both repayment time and total interest costs.

Common Myths About Minimum Payments

Many people misunderstand how minimum credit card payments work.

Myth: Paying the Minimum Means the Debt Is Under Control

Making the minimum payment keeps your account current, but it doesn’t necessarily reduce your debt quickly.

Myth: Minimum Payments Prevent Interest

Interest may continue to apply to any remaining balance according to your credit card agreement.

Myth: Small Balances Don’t Matter

Even relatively small balances can become expensive if carried for long periods while interest continues to accumulate.

Myth: Paying the Minimum Is Always the Best Option

Minimum payments provide short-term flexibility, but paying more whenever possible generally helps reduce debt faster and lowers total borrowing costs.

Common Mistakes to Avoid With Credit Card Payments

Credit cards can be useful financial tools, but certain habits can make debt more expensive and difficult to repay.

Some common mistakes include:

- Paying only the minimum every month for long periods.

- Continuing to make new purchases while carrying a large balance.

- Missing payment due dates.

- Ignoring your monthly credit card statements.

- Using credit cards for purchases you cannot realistically repay.

- Treating your credit limit as extra income.

- Failing to create a repayment plan.

Avoiding these habits can help you reduce borrowing costs and improve your overall financial health.

Tips for Managing Credit Cards Responsibly

Responsible credit card use can help you avoid unnecessary debt and maintain stronger financial habits.

Consider these practical tips:

- Pay your full statement balance whenever possible.

- If you can’t pay the full balance, pay more than the minimum whenever your budget allows.

- Make payments on or before the due date.

- Review your monthly statements carefully.

- Avoid unnecessary impulse purchases.

- Keep your spending within a realistic budget.

- Build an emergency fund to reduce reliance on credit during unexpected situations.

Small improvements in how you manage your credit card can produce significant long-term financial benefits.

Frequently Asked Questions

Is paying the minimum considered a late payment?

No.

If you pay at least the required minimum amount by the due date, your payment is generally considered on time according to your card agreement.

Does paying only the minimum eliminate my credit card debt?

No.

The remaining balance usually carries forward to the next billing cycle, and interest may continue to be charged according to your card’s terms.

Can paying more than the minimum help?

Yes.

Paying more than the minimum generally reduces your outstanding balance faster, shortens the repayment period, and lowers the total interest you may pay over time.

Is it ever okay to pay only the minimum?

During temporary financial hardship, paying at least the minimum can help you keep your account current and avoid missed-payment consequences.

However, increasing your payments once your financial situation improves is usually a better long-term strategy.

Should I stop using my credit card while paying off debt?

Many people find it easier to reduce their balance by limiting new purchases until existing debt has been repaid.

Whether this is appropriate depends on your financial situation and ability to manage credit responsibly.

What should I do if I can’t afford my credit card payment?

If you’re struggling to make payments, review your budget immediately and contact your card issuer as soon as possible to discuss available assistance or repayment options.

Acting early may provide more options than waiting until payments are missed.

Conclusion

Paying only the minimum on your credit card may help you keep your account current, but it is generally one of the slowest and most expensive ways to repay debt.

Because a significant portion of each payment may go toward interest instead of reducing your principal balance, carrying a balance for a long period can substantially increase the overall cost of borrowing.

Whenever possible, paying more than the minimum can help you reduce your balance faster, lower the amount of interest you pay, and improve your financial flexibility.

Combining larger payments with a realistic budget, careful spending habits, and a commitment to avoiding unnecessary new debt can make it much easier to become debt-free.

Remember that credit cards are most beneficial when used responsibly.

Understanding how minimum payments work allows you to make informed financial decisions, reduce borrowing costs, and build stronger long-term money management habits.